Chapter 2: Back to The Drawing Board

We left off in the last article with having just found out that the budget our builder gave us was $400k over and we were supposed to start building in 3 weeks. If you haven’t read the beginning of the story, I recommend you do that first Here.

Once we found out our house was too expensive to build, we put a stop on moving forward with construction until the beginning of 2023. We needed to go back to the drawing board and cut square footage and rethink our life.

From this point forward we would be paying the architect and engineer hourly to make changes to our plan because we had already approved the plans. We approved the plans because we thought we would be within our budget. We thought we would be under budget because our builder didn’t give us any indication that we wouldn’t. We ended up spending an extra $4,000 on architectural and engineering plans.

My initial response to the builder after he sent the budget was, “How did we end up so off in the initial estimates? $970k? That’s almost 400k over.” And his budget was still missing some big items like concrete flatwork and flooring. And many of the numbers weren’t actual bids, just guesses based off a recent house he did that was a totally different style. And the lumber was based off lumber prices during the big COVID surge but at this point lumber prices had dropped way down.

He didn’t respond to my email.

A couple days later we photoshopped the blueprints showing what we decided to cut. At this point, we were just shooting from the hip because we had no guidance from the builder on how to get the cost down except what he mentioned a week prior about cutting the basement and 3rd car garage. Again, there wasn’t enough sitting down with the builder and architect to figure this problem out. It was just skim emails with rushed decisions. We lived 3 hours away from the builder at the time, which didn’t help.

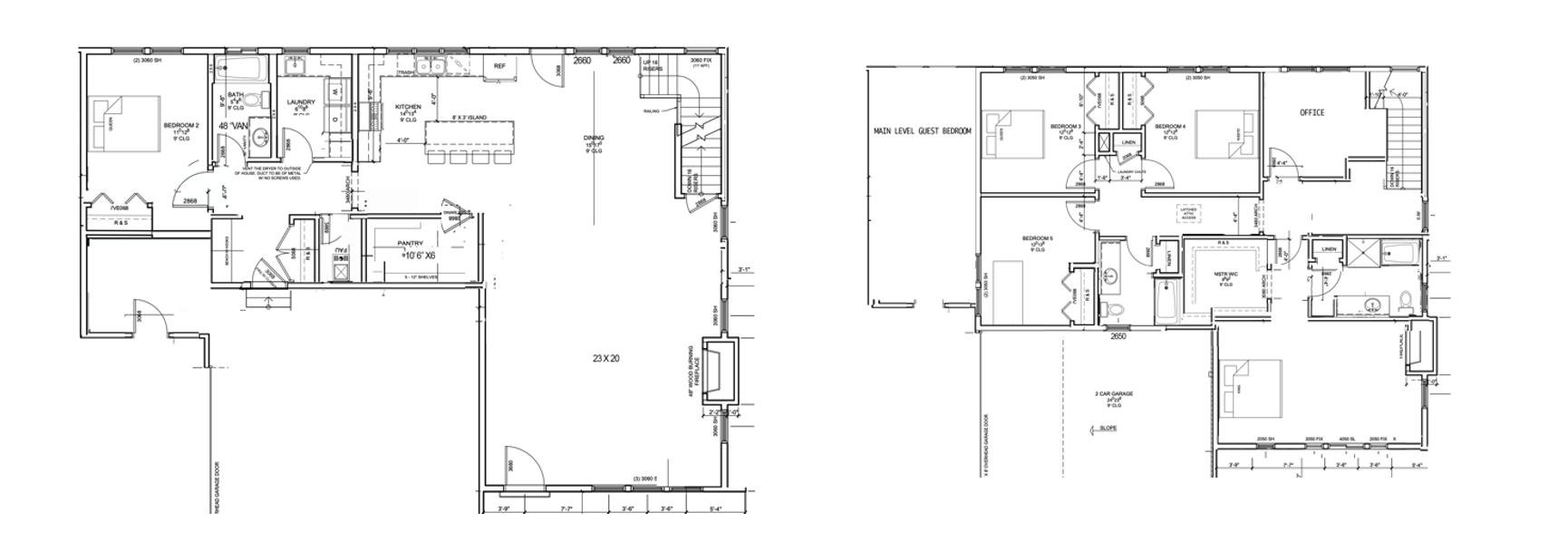

The cuts we decided to make included eliminating the whole right wing of the house which included a second living room/play room and my large office above on the second floor. Instead we converted the storage area upstairs to an office and made the guest bedroom on the main floor double as our play room for the kids. We also got rid of the 3rd car garage. And we made the basement half crawl space and half basement (worse idea ever). Thank goodness we reverted back to a full basement before we started building. More on that later.

You can see our adjustments to our floorplan here a and compare to the plan in Chapter 1:

So in total, we cut 632 square feet above ground, 600 square feet of basement and 264 square feet of garage. So that should have cut around $150k from the budget based on the cost to build according to the first budget. Wait until you see the next version of the budget our builder sent us based on the smaller house…

So by September 28, only 4 days later, the architect had redone the plans based on our sketch. 4 days is not enough time to revamp your house that is $400k over budget! We should have spent weeks figuring this out, meeting with the builder and architect and getting actual numbers on cost before paying the architect to keep making changes.

After the architect sent over the updated plans, our builder responded saying that we likely needed to cut the whole basement to bring the cost down. He kept zeroing in on the basement as being the biggest area contributing to the cost. And it was only later that we realized the excavation was actually cheaper per square foot to dig the basement then it would have been to do slab on grade. Our neighbor across the street was building at the same time and he spent more on excavation per square foot for his slab on grade then we did on the basement because he still had to dig 6 feet down and re-compact soil all the way back up to prepare it for a foundation since we have collapsible silty soils here. We found this out before we started digging and luckily added the full basement back in at the last minute months later in 2023.

Of course concrete would be more expensive for the basement and other materials if we finished it but in the end, the basement was not the thing that put us over budget. That’s why at Finding Home, basements are standard. For one, a basement foundation is a more structurally sound foundation because it’s built on more compacted soil deep down and the wall structure helps distribute forces, like an earthquake better than slab on grade. And earthquakes are a risk in Utah. Basements also give you ample storage space and the ability to expand your living area later as your family grows.

So back to our conversation with the builder about our budget. In his next email, he gave us numbers of the average cost to build in our area and also sent over a pdf guide with a formula on how to calculate the cost to build for our house. He’s just now sending this over?? He’s just now starting the conversation of estimating the cost to build, after we already approved the architectural plans, and the engineer was working on their plans? This conversation should have been taking place during the drafting stage of our architectural plans.

In my response, I mentioned that interest rates were going up and our budget was dropping even more so we just needed to pause everything until the new year. But the next day, I sent additional tweaks to the architect. We should have spent months mulling over this. At this point, I honestly thought that we wouldn’t get charged extra for these changes. Our builder had mentioned in a text to me that the architect can easily make changes to shrink the house and is very accommodating, so I interpreted that as he must not be charging us extra money to make these changes. In the end we got an invoice from the architect for the extra time spent.

I also assumed because we basically handed the architect a floor plan initially that he just had to copy and paste, that the time he saved in the initial phase of designing the larger house banked him extra time to use in these changes. Wrong. So, I didn’t ask for confirmation on whether he was charging us and they didn’t bother to share that detail either. Bad communication on both sides.

At this point, on Sept 30, we considered our changes done and they sent the plans over to the engineer so they can start redoing their plans to match the smaller house. Our builder had told us that the engineer didn’t even get started yet so we thought that wouldn’t cost any extra. Wrong again. We found out later that the engineer was almost finished at the time we sent the updated architectural plans. They already drafted their plans based on our bigger house and charged us extra to shrink it. The architect and engineer’s initial pricing was based on the square footage of the house. So even though our house ended up being 1200 square feet less including the basement and garage, we had to pay based on the original square footage PLUS hourly for all the changes.

Also, we still didn’t have an updated budget yet, but we were going to pay the engineer to update their plans! And we approved the architect’s changes! Insanity!

Over the next month there was a lull. No communication had happened between us and the builder and we were just waiting for engineering to finish their plans so the builder could update his budget. There’s no reason why the builder couldn’t update his budget without those. This wasn’t a final budget, we just needed an updated ballpark budget but we couldn’t even get that.

On October 28th our builder followed up with the engineer to ask where the plans were.

On October 31, our builder said he would have engineering plans soon and then he would get bids in the middle December so they’re fresh by January. He’s assuming and we’re assuming that once he gets bids, we’ll magically be under budget and can start building right away. We still weren’t going to know until January what our updated budget was once I closed my income for the year. I’ve always been self-employed so qualifying for a mortgage was not an easy process and they based it off 2 years of tax returns. In 2022 I earned a lot more money than 2021, so once the year ended I would get a new tax return and be able to raise our house budget but I still didn’t know what that would be until our lender reviewed everything.

On November 8, the engineering plans were finished. On December 1 is when we got our first update from the builder on our budget and he said he shaved it down to just below $900k. But his email attachment of the budget spreadsheet was empty, no actual numbers. I asked for the actual budget spreadsheet but no response. For the rest of December, we had a few emails regarding finishing choices and on December 29th is when he actually sent the new budget. The total budget, after waiting a couple of months and making all those changes, was $933k. That was only $40k less and we needed it to be $400k less!

And there were still no budget numbers for flooring or plumbing fixtures. These items combined ended up costing $60k, but our builder and us weren’t concerned at the time, again blinded by the hastiness to get started.

By this point, I knew that in January, once I did my taxes, I would likely qualify for $800-$850k total including the land we already owned. The downpayment on our lot would rollover into the downpayment on the house. So, because our qualification amount would likely go up in January, we started to be somewhat okay with the budget, which was so dumb. Just because I can qualify for that high of a mortgage doesn’t mean we should get it. My income by that point was showing us that if our mortgage was $850k then we would have $3k extra in income each month after all our bills. That was a comfortable enough buffer but what we didn’t foresee was the extra $60k in debt that we would be taking on soon after moving in and my huge drop in income that occurred because of devoting way more time to our house build than we anticipated. So we proceeded forward, not playing it safely enough. I probed our builder to keep looking for where items could be dropped because I was still seeing entire sections of the budget that was unchanged from the previous one even though we cut 1200 square feet from the square footage of our house. I kept thinking, what was the point in cutting that space if the budget barely budged?

In hindsight, I realized that the first budget he sent was missing so many actual bid numbers that it was likely way underestimated and that’s why when he started getting bids, the updated budget was only a little bit less. If you’re building a custom home, you need to make sure your builder is very precise at estimating cost even if he’s waiting on actual bids so he can better help you through the design process. What helps a builder have an easier time estimating costs accurately is if he or she is only willing to build a certain style of house and isn’t going outside those parameters. At Finding Home, we only build traditional American colonial style houses with a semi-open concept. We will not go outside our expertise because then we won’t be able to accurately scope out the project. Our builder for our home, was going way outside his comfort zone with the style of our house compared to what he was used to building. He should have realized that and said no to our project, and we should have realized that and never signed a contract.

We realized only later that certain complicated features of our house design were totally not necessary and drove up the cost a lot. We’ll get into those in later articles.

A few days later, on January 5th, 2023 our builder sent another updated budget. He now had flooring in there, but his flooring subcontractor based the bid off the original larger house…this really started to make it clear that our builder was not organized enough to keep track of the most recent version of the plans and was still sending people the wrong ones. So, we decided to go into the budget ourselves and adjust numbers down based on the square footage reduction.

What proceeded next, on January 11th was ridiculousness at its finest, from us and our builder. I redid the budget since we lost trust in our builder to get accurate numbers. I reduced areas like flooring and concrete that were heavily dependent upon square footage to match the smaller house plan. Then I eliminated interior painting and tile install and labelled those as “sweat equity” meaning we would do the labor for those things ourselves. At the time, we didn’t realize that the bank wouldn’t allow any budget items to be eliminated because of sweat equity. They needed a budget that included hired labor for everything.

Our builder suggested to just plan to use contingency to cover those areas but in the end agreed to our budget without pushback. Never plan to use contingency to cover anything! We thought we would have our $60k in contingency intact to be able to cover the cost of our fence, landscaping and other items being under. Bad move!

After this conversation with our builder, we were telling him, we couldn’t qualify for more than $915k and our builder said to just “submit what budget we want around $915k” and he’ll sign it. That was massive negligence on his part and ignorance on ours. In our minds, we were convinced that there was no way a 3,000 square foot house would cost $900k with land. Was inflation really that bad? It was. But we also designed a house that costed a lot more than it needed to. A combination of unnecessary framing structures, material selections that could have been different, wasteful building processes, mis-management and poor workmanship, is what sent us way over. Again, we didn’t know what we were doing and were trusting that our builder did.

On January 11 by the end of the day, we finalized the budget and sent it to our bank for the final qualification process.

We learned later that the numbers we adjusted in the rough-in phase of construction to match the smaller house plan, ended up being fairly accurate but the cost of most items in the finishing phase were way off. Many of the materials we chose for finishes were materials our builder was not familiar with, revealing that he was used to using more production grade materials. We wanted real stone veneer on the front, hardie shake siding, real hardwood flooring, and solid brass doorknobs to name a few. He didn’t understand what those would cost and we found out later that his allowances were not based on those materials. He thought it was okay to not get accurate bids on the finishing items and to just put in allowances. And we can finalize later in the build what finishes we want. Don’t do that ever! Get bids one everything! You must decide all your finishes up front if you want an accurate budget.

There are many things we would have changed in our finishes if we knew what the actual cost was going to be. One cringe example is the extra $15k we spent on our roof. Our builder was very passionate about us getting an aluminum shingle roof. He liked promoting them and thought they were the only way to go with roofing, regardless of house design. We never questioned him on it. This company claimed that their shingles had 100-year warranties on them. We found out later, there are so many exclusions, you can hardly call it a warranty. Also, who is ever going to live in their house for 100 years? You’ll learn more details about the harrowing nightmare that the install process of our roof became. It was such shoddy work and took forever, which made the extra expense of it even worse. And I can’t even climb on it, because it’s too slick for our roof pitch. And it didn’t actually boost our appraisal value even though it’s more energy efficient. If the budget was more accurate and we had known what real hardwood would cost for example, we would not have paid the extra $15k on the aluminum shingle roof and instead put that towards the flooring that went over budget.

We told our builder we wanted solid wood baseboards and casings. His estimate was based off MDF trim. We told him we wanted hardwood flooring that needed to be finished on site to have the right color, and he got a bid for pre-finished instead. We wanted real stone veneer for the front exterior, and his estimate was based off manufactured stone veneer and the list goes on. We thought his numbers were based off our requests but in his mind, he thought he would convince us to select the lower quality finishes. We should have asked and probed for confirmation of where his numbers were coming from. We should have slowed down and let our brains process what was going on for a second because we just weren’t thinking clearly. I was eager to close on our loan, because with being self-employed, I needed to show not only recent tax returns but my income from the most recent month. And I was afraid it this got delayed too long that I could end up with a bad income month and it would interfere with our qualification. I let fear and anxiety get the best of me.

That’s why part of our mission at Finding Home is to help people who are self-employed find an easier path to homeownership.

Over the next month, the mortgage qualification process for us got increasingly stressful, as we were still waiting on actual bids on a few items, had to revise the budget several more times, and we found out that our builder was on our bank’s “Don’t Build With Again List.” Uh oh…We’ll get into the details of that surprise in the next post.

Thanks for reading! If you’re wanting to build a home, feel free to reach out to us and ask about how we approach the budgeting process to ensure you have accurate numbers and can make the right decisions. We learned the hard way how NOT to budget and we don’t want you to make the same mistakes.